Quarterly Economic Update: Third Quarter 2025

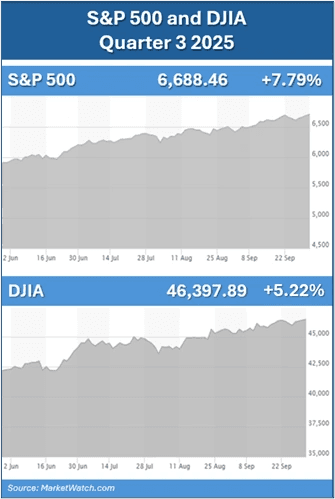

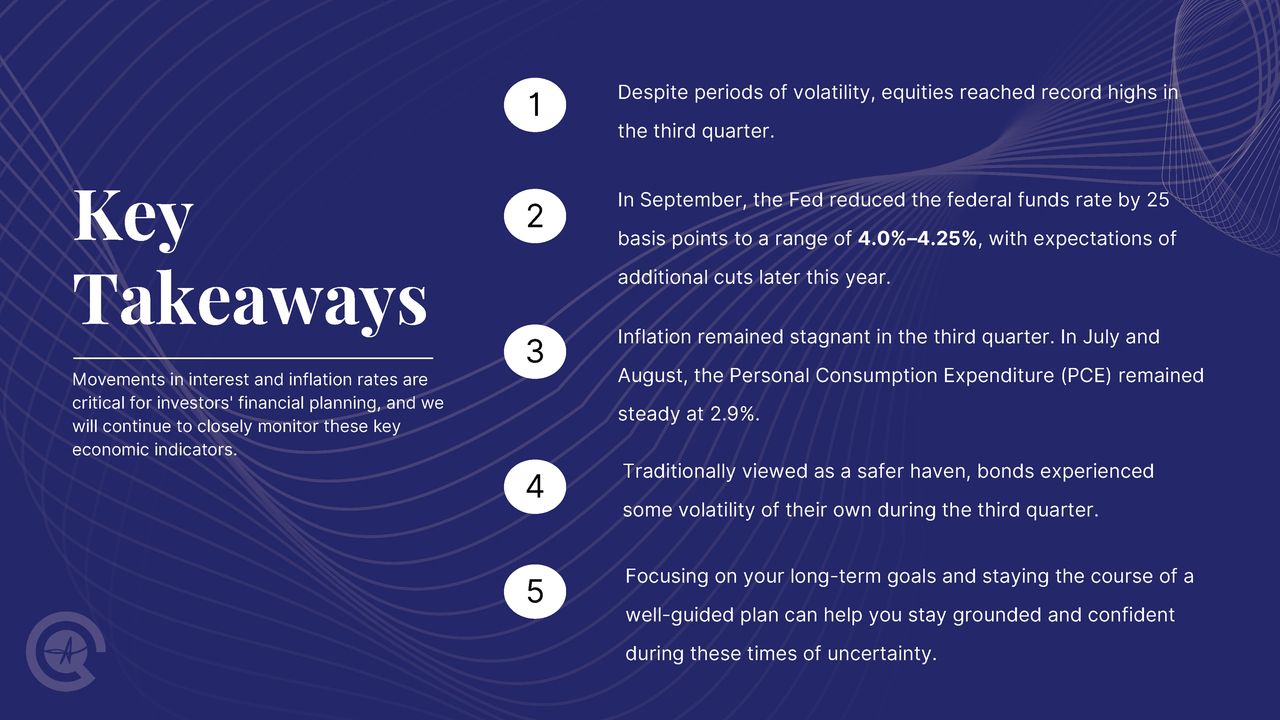

Resilience illustrates the ability to withstand challenges or recover quickly from difficult conditions. Resilience can also be used to describe U.S. equity performance over the past year—including the third quarter, as markets surged past record highs despite numerous potential sources of volatility. Largely fueled by optimistic investor sentiment around the AI boom, robust corporate earnings, and expectations of further interest rate cuts, the U.S. stock market continued its bull run that began in early 2023. The artificial intelligence (AI) boom is continuing to drive growth in the technology sector, dominated by the “Magnificent 7” (Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla). In addition to the AI boom, healthy corporate earnings and the Fed lowering interest rates for the first time this year all helped the market rally. The S&P 500 gained 7.79% in the third quarter, closing at 6,688.46. Year-to-date, as of September 30, the S&P 500 is up almost 14%. The Dow Jones Industrial Average (DJIA) closed at a record high, gained 5.22% and ended the quarter at 46,397.89. Year-to-date, as of September 30, the DJIA is up over 9%.

Anthony Collica

Executive Director of Wealth

Table of contents

Share

Since the recovery from the quick correction we saw in April, the market has rallied. While investors have a bullish outlook, a backdrop of caution and uncertainty still remains. During the third quarter, the U.S. job market showed signs of cooling but remained strong. While a prolonged government shutdown could increase the unemployment rate in the near future, as of August, the unemployment rate was slightly elevated to 4.3%, the highest in nearly four years. (Source: Bureau of Labor Statistics; 9/5/25)

Overall, the data continues to support a positive long-term view for equities, however there is still an undercurrent of caution. As always, our role as financial professionals is to actively monitor developments and confirm that your portfolio remains aligned with your time horizon, risk tolerance, and financial goals. Our commitment is to keep you informed, proactive, and resilient—just like the markets themselves.

Inflation & Interest Rates

Key Points:

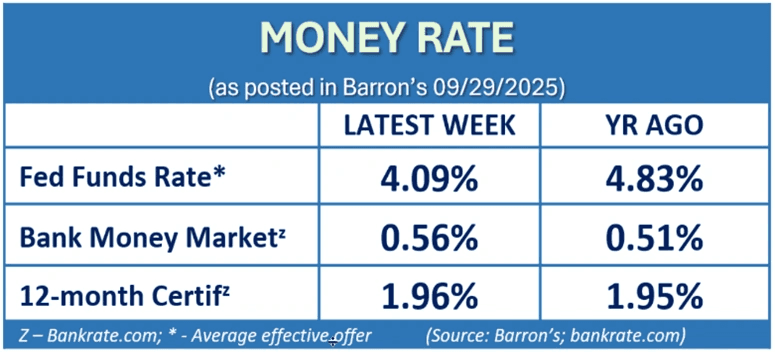

Interest rates were lowered by 25 basis points down to 4.0 – 4.25% in September, the first rate cut for the year.

The Fed is currently forecasting more rate cuts for 2025.

The core Personal Consumption Expenditure (PCE) remained steady at 2.9% in August.

In its September 17, 2025, press release, the Federal Reserve noted: “Recent indicators suggest that growth of economic activity moderated in the first half of the year. Job gains have slowed, and the unemployment rate has edged up but remains low. Inflation has moved up and remains somewhat elevated.” (Source: Federal Reserve Press Release, 9/17/25)

In September, The Fed lowered interest rates for the first time in 2025, establishing a new target range of 4.0% to 4.25%. Looking ahead, there are two more FOMC meetings scheduled for the remainder of 2025. While uncertainty surrounding the economic outlook persists, the Fed has indicated that additional rate cuts are possible this year, though not guaranteed. (Source: Associated Press; 9/24/2025)

In August, the core Personal Consumption Expenditure (PCE) remained steady at 2.9%. The annual Consumer Price Index (CPI) which excludes food and energy was 3.1%, according to the Bureau of Labor Statistics. (Source:cnbc.com; 9/29/25)

Movements in interest and inflation rates are critical for investors' financial planning, and we will continue to closely monitor these key economic indicators.

The Bond Market and Treasury Yields

Key Points:

Bonds, which can be viewed as a safer haven for volatility, were not exempt from volatility in the third quarter.

The current direction of bond yields remains unclear, however, with the Fed anticipating lowering interest rates again, we could see existing bonds rising in value.

Bonds are typically a more stable option for investors during times of uncertainty. Lately, however, bonds have been reactive. As the quarter ended, treasury yields responded favorably to the solid data of the U.S. economy. The benchmark 10-year treasury yield settled at 4.12% to end the quarter, while the 20- and 30-year ended at 4.58% and 4.73% respectively. (Source: treasury.gov resource center)

We consider using bonds when they are appropriate for portfolios, and when we do, there are several things we take into consideration, including a client’s risk tolerance, time horizon, and overall investment goals. Bonds can be an integral part of a well-diversified portfolio and offer stability during times of market decline. However, please remember, while diversification in your portfolio can help you pursue your goals, it does not ensure a profit or guarantee against loss.

Investor’s Outlook

Key Points:

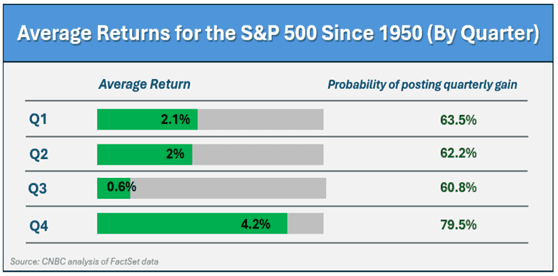

Historically, the fourth quarter has been the strongest performing quarter for the S&P 500 since 1950.

Vigilance is critical for the savvy investor, as volatility remains. Having a proactive planning approach that includes an emergency fund and a well-diversified portfolio that takes into consideration your risk tolerance and time horizon is still advised. A long-term approach to your financial goals and avoiding diversions is typically the best path.

While no one has a crystal ball, and past results do not reflect future ones, it’s interesting to note that based on historical data for the S&P 500 index, the fourth quarter is the strongest-performing quarter for equities. Since 1950, it has delivered the highest average return and the highest probability of posting a gain. (Source: finance.yahoo.com; 9/25/25)

The chart in this report reflects returns since 1950, which includes several very difficult 4th quarters, including October of 1987 when the market collapsed and had its worst single day in history. When studying the returns, almost 80% of the time, Q4 ended the respective year on a high note.

Many continuing uncertainties surround the economic environment, and our goal is to continue to focus on key factors that could affect your personal situation. As of this writing, equity markets continue to look strong, but some key items to keep watching as we finish the year are:

The chance of an economic slowdown.

The direction of inflation and interest rates.

The possibility that stocks are overvalued.

The new tax law, and

Geopolitical conflict.

As the saying goes, “Everything is fine until it’s not.” Volatility is still prevalent and may continue for some time. As we look to the future, being vigilant is crucial for savvy investors. Remember, while volatility can have negative implications, it can also present opportunities, therefore, we would like to remind you once again that equities are long-term investments.

2025 continues to be a year of change for the U.S. As your financial stewards, we closely monitor areas that we believe are important to your financial well-being.

As always, please inform us of any changes to your circumstances, including health issues, any sale of property, or adjustments to your risk tolerance or time horizon. We encourage you to share any concerns, ideas, or potential decisions with us before taking action. Financial choices often have tax implications and other considerations, therefore, the more we understand your unique situation, the better positioned we are to offer tailored guidance.

Our team is here to help you with every step of your journey toward your financial goals. Please feel free to reach out to us with any questions or concerns you may have. We greatly value the trust and confidence you place in our firm and look forward to continuing to serve you.

Sources: cnbc.com; barrons.com; marketwatch.com; treasury.gov; Bureau of Labor Statistics; Federal Reserve; The Associated Press; U.S. Department of Treasury. Contents provided by the Academy of Preferred Financial Advisors, 2025